The low-interest rates over the last 6 years created an unbalanced risk-to-reward ratio which ballooned already over-capitalized private equity and venture capital markets; inflating valuations and producing a bubble. Hybrid investment in the form of debt plus equity allows investors a better compromise of risk to reward in today’s startup market situation.

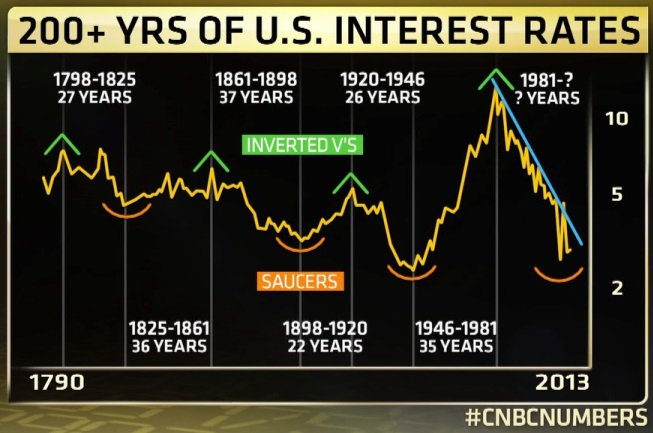

Moderate risk-taking investments provide the capital foundation for innovation, economic growth, and prosperity. Mispriced risk, however, can be catastrophic. Overcapitalization is driving the inflated valuations and oversized investment checks that are prevalent in today’s market. Over the past 6 years, interest rates have remained at historic lows, fueling the economy with cheap capital. Low fixed income yields have pushed investors to search for high returns in the riskier equity markets. To make matters worse, a number of additional catalysts will lead to a sell-off and loss in the VC industry within the next 2-3 years.

Source: Yahoo Finance

Overinflated valuations are the largest catalyst. These valuations resist rebalancing due to the illiquid nature of VC investments. VCs often invest in companies that have never generated profits (or even revenue in some cases). The capital invested is typically through investment instruments in the form of convertible notes or straight equity. Investors’ capital is generally locked up for a period of 5-10 years and turns liquid only when equity positions are bought out. Until then, an investor’s only metric for investment performance is based on either priced rounds or comps.

Conventional VC pricing methodology is flawed, with incentives that are improperly aligned and a process that provides no counter-weight to create valuation equilibriums. Most priced rounds typically consist of additional investments from similar (and/or existing) investors at each round, and it is in the interests of both new and existing shareholders for the valuation to increase at each capital event.

Average startup valuation is $4.2 million

The going market rate for a new company’s valuation with an idea (pre-revenue) is in the $1 – $5 million range with an average around $4.2 million . This means, a company looking to raise $200K to build its first line of code would part with 4-20% of its equity.

Source: Angel List

Let’s assume that same company, one year later, is successful and can show sales of $500K and an annual burn of $300K – it looks at raising an additional $500K. The company compares itself to another company in a similar space and industry that shows the same economics and raised a $500K round at a $6 million valuation. Our company points to that valuation to justify the price of their current raise and, additionally, argues why they are better positioned to justify an even higher valuation, enabling them to retain more equity for the same raise – the deal gets done at an $8 million valuation. Current investors (excluding dilution), would mark their investment as having doubled in one year. Our company, with sales of $500K and a loss of $300K, it is now valued at $8 million; all due to the current state and structure of the VC financing market.

Keep in mind that no cash has actually been returned to any investors and no sale has been made for full price. In this case, the sum of the parts does not equal the whole. This is the fundamental problem and it will come back to haunt many of these companies and VCs at the end of their investment period.

Why invest in losses?

Let’s go back to the fundamental elements present in today’s economy: low-interest rates due to government intervention led institutional investors to allocate capital towards riskier assets, generating larger returns to justify their fees. It is a seller’s market, in favor of companies raising capital, and because recent historical valuations continue to grow “on paper”, investors are willing to invest at astronomical valuations regardless of a company’s economics.

To make matters worse, many platforms enable both accredited and non-accredited investors to invest in companies they never talk to, meet, or understand. These platforms will carry out the due diligence on your behalf and offer you documents if you ask, but they are also incentivized to promote transactions to feed their revenue model. For many novice investors, the “invest in 10 companies and 1 win will cover my loss” mentality is enough to deploy capital on recent historic valuation performance; the same valuations we just learned are not necessarily a function of a company’s economic performance. Betting on a self-fulfilling prophecy where the first company to walk the path becomes the benchmark only reinforces the cycle and dilutes the next investor.

Snowball effect

In order for all investors to get their money back and actually realize their perceived returns, there has to be an exit or buy-out at that final valuation. Companies are approaching private equity groups, the IPO market, and potential acquisitions proudly waiving a $100 million valuation and expecting a check. While a few companies will make it through and justify their valuations, many companies will not come close to having the revenue, cash flow, or profitability to warrant such an exit value. Private equity funds and larger companies are correctly questioning valuations and only bidding a fraction of the asking price.

What is the result? A company on paper that showed growth for 7-10 years with an ending valuation of $100 million ends up selling at $50 million, creating a huge loss for the investors. This will most likely affect later-round investors, who are usually the ones writing the larger checks. Once this happens VC firms will struggle to redistribute capital to their LP’s, forcing a sell-off of other portfolio companies and creating a snowball effect throughout the industry with large selloffs at discount prices.

The case for hybrid growth capital

LunaCap Ventures’ investment thesis enables us to generate yield and return capital regardless of paper valuation, all while maintaining exposure to the potential upside of the VC world. LunaCap invests with a hybrid growth capital instrument. We provide a non-convertible term loan with multi-year amortization and equity participation, typically in the form of warrant coverage. The term loan, and regular payment requirement, simultaneously filters for companies that prioritize cash-flow and provides our economic foundation. It enables our investors to receive cash yield on their capital allocations to LunaCap. The term loan mitigates risks with a short term maturity, and as protection, often sits senior on the capital table – providing downside protection. Additionally, our warrant coverage is generally 5 times smaller than the equity a company would have to part with in a conventional VC investment of comparable size, yet helps drive an average LunaCap return commensurate to that of early stage investing.

On the company side, overall cost of capital is much lower than the classic VC model when accounting for the value of the 80% equity retained. For LunaCap, this provides the most important filter. If the company believes they are going to do extremely well, then our debt instrument becomes very cheap. If the company does not believe they are going to grow, then we are expensive and it may not make sense to take our investment. As a rule of thumb, if you don’t believe in yourself as a company, I don’t think we should be partners in the first place.

Averages and exceptions

There are about 500 active VC firms in the United States and a number of top VC firms will continue to enjoy great success. In general, I caution one should understand the value of the company assessed before investing. Make sure the valuation is justified on its own merits and not because someone else is willing to invest at the presented terms and valuation. You can do well riding the wave for a bit, but that is a risky game to play. I love the start-up space and highly respect any VC firm or individual willing to take a bet on a team or company. I have full faith in my colleagues and peers who are fund managers and investors across the industry; they are investing with good conscience and a deep understanding. However, it is also important to highlight the dynamics and forces in play, informing investors’ decisions for both their benefit and that of their portfolio companies.